IFA41 – Weighted Average Inventory (Periodic) & Method Comparison – Intermediate Accounting

🛍️ Products Mentioned (1)

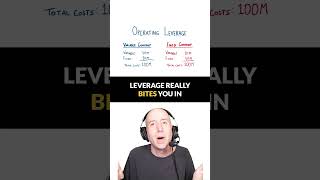

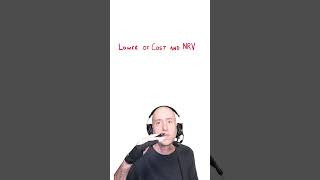

Download the Workbook: http://www.tonybell.com Unlock 100+ Members Accounting Tutorials: https://www.youtube.com/channel/UCNFClg6mzfZ5ixpuH9c7f1A/join In This Video: We wrap up our exploration of cost flow assumptions with Parts B and C of Problem 8-4A. First, we apply the Weighted Average method under a Periodic inventory system for ABC Company, calculating a single, blended average cost for the entire month to determine Ending Inventory and Cost of Goods Sold. We record the necessary journal entries and month-end adjustments, including the bonus shrinkage scenario. Finally, in Part C, we place our results from FIFO (8-2A), LIFO (8-3A), and Weighted Average (8-4A) side-by-side. We compare the Gross Profit generated under each method and explain the underlying theory—specifically, why FIFO yields the highest profit, and why many American companies intentionally adopt LIFO to achieve the lowest profit. Module Overview (IFA35–IFA41): This module explores Inventory valuation and tracking in depth. We will examine complex cost flow assumptions, analyze the impact of inventory errors, and apply valuation rules like Lower of Cost and Net Realizable Value (LCNRV). We will also cover inventory estimation techniques, such as the gross profit method and the retail inventory method, while highlighting key differences between US GAAP, IFRS, and ASPE.